By Keeping Current Matters

A survey by Ipsos found that the American public is still somewhat confused about what is actually necessary to qualify for a home mortgage loan in today’s housing market. The study pointed out two major misconceptions that we want to address today.

1. Down Payment

The survey revealed that consumers overestimate the down payment funds needed to qualify for a home loan. According to the report, 36% think a 20% down payment is always required. In actuality, there are many loans written with a down payment of 3% or less.

Many renters may actually be able to enter the housing market sooner than they ever imagined with new programs that have emerged allowing less cash out of pocket.

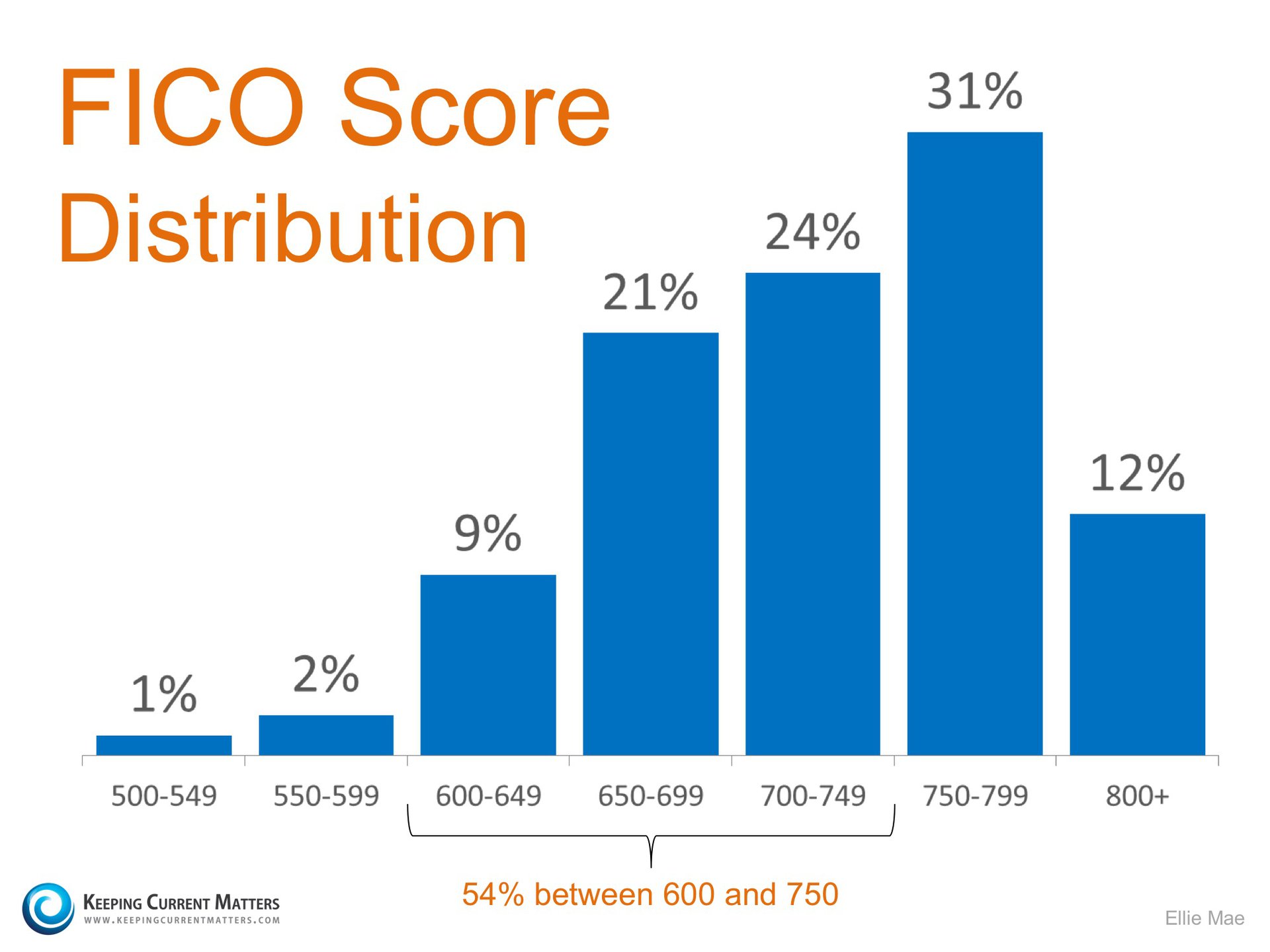

2. FICO Scores

The survey also reported that two-thirds of the respondents believe they need a very good credit score to buy a home, with 45 percent thinking a “good credit score” is over 780. In actuality, the average FICO scores of approved conventional and FHA mortgages are much lower.

The average conventional loan closed in March had a credit score of 753, while FHA mortgages closed with a 685 score. The average across all loans closed in March was 722. The chart below shows the distribution of FICO Scores for loans approved in March.

Bottom Line

If you are a prospective buyer who is ‘ready’ and ‘willing’ to act now, but are not sure if you are ‘able’ to, sit down with a professional who can help you understand your true options.